What Time is it?

The AI Economy Has Multiple Clocks

## Editorial

## What Time is it?

The AI Economy Has Multiple Clocks

Grok 4.5 arrived this week with a simple promise: near-frontier intelligence, faster and cheaper. A lot cheaper.

Elon Musk called it “Opus-class, but faster, more token-efficient and lower cost.” xAI called it its “first model trained specifically for coding and agents.”

That is a product launch. It is also a price signal. And OpenAI launched ChatGPT 5.6 as a far more efficient user of tokens than Anthropic. Costs again. Everybody is talking about the price of tokens.

This week I kept trying to find one theme and kept finding several. That is usually a sign that the theme is hiding one level higher.

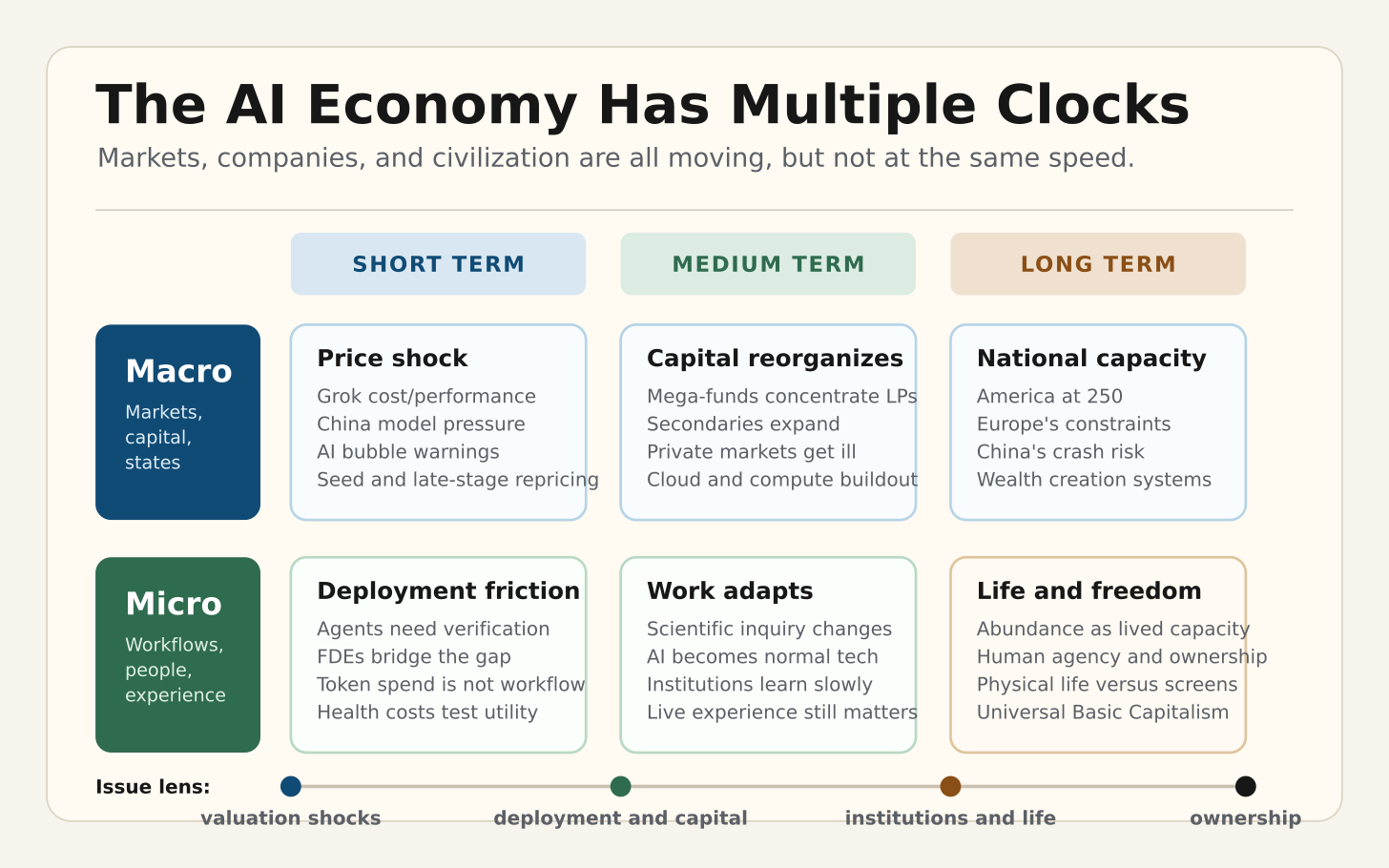

AI is not one story. It is a market story, a deployment story, a capital and infrastructure story, and a civilization story. And they are all on different timelines. The mistake is to force all of those clocks to show the same time.

The first clock is short term - price

The short term clock is governed by price. The Grok 4.5 argument is not only whether it is smart. It is whether it is smart enough at a price that changes buyer behavior. Latent.Space’s coverage puts the launch on the cost/performance frontier, not merely the benchmark frontier.

That matters because price is the first way a technology becomes economic. A thing can be brilliant and irrelevant if it is too expensive to use often. A thing can be slightly less brilliant and transformative if it is cheap enough to be everywhere.

The same price clock shows up in China. CNBC reports that Chinese models have accounted for more than 30% of tokens used by U.S. companies every week since February 8, peaking at 46%. That is not driven by ideology. That is logic and math driving procurement.

If a model is 60% to 90% cheaper and good enough for a large class of tasks, engineers will route work to it. They should. In the short term, the market is discovering that “frontier” and “useful” are related but not identical categories.

The venture version of the price clock is valuation. Terrence Rohan calls the current top 5% of seed deals “the worst asset class in venture” and summarizes the trade as “Seed risk at Series B prices.” Risk has not moved down as fast as price has moved up. Seed companies are still seed companies. They can still fail like seed companies. But the top of the market is starting to price some of them as if the future has already happened.

So yes, there is froth. Treasury analysts are apparently worried enough to model an AI pullback as a financial-stability issue. Samir Kaji is right that venture is living through a genuine AI supercycle and an obvious late-cycle bubble at the same time. Both can be true. Most AI companies can be overvalued and a few can still become the largest companies ever created.

That is the first clock. Markets are repricing AI in real time.

The second clock is also a short term one - deployment.

This is where the AI story gets less glamorous and more important. Aaron Levie says enterprise IT leaders are moving away from token counts as the main adoption metric and toward business outcomes. That is inevitable. Nobody should care how many tokens a company consumes if the workflow stays the same, the customer experience stays the same, and the P&L does not move. So what to deploy is the form taken by market penetration. Anthropic is a net loser in this equation.

The hard part is that enterprises do not run as neat prompts. They run through silos, legacy systems, messy permissions, fragmented data, and people who are accountable when something breaks. Levie’s point is that agents are most useful when they cross those boundaries. That means the problem is no longer just model capability. It is ownership, adoption, data access, measurement, and responsibility.

OpenAI’s ChatGPT Work announcement makes that shift explicit. The pitch is no longer a smarter chatbot. It is an agent that can gather information across apps, create sheets, slides, docs, and web apps, and stay with complex projects for hours. OpenAI says more than 5 million people use Codex every week and more than 1 million now use it outside software development. That is the tell. Coding agents are becoming work agents. And the consolidation of Codex and Chat into a single new app (with an old name - ChatGPT) that includes ‘Work’ shows OpenAI means business (pun intended).

Nate’s piece on agent trust says the same thing from a different direction. The answer is not waiting for a model that never hallucinates. The answer is verifying the work, not worshipping the model. His $8 multi-agent website run is funny because it is so familiar: one agent fabricated thirteen quotes and certified the work as flawless. The system only worked because other agents caught the failures, documented them, forced rework, and verified the output. This is a loop, and if you are not using it, you should be.

Real institutions adopt new capabilities, not simply by believing, they inspect.

The Bun rewrite is the same lesson in production engineering. Jarred Sumner says Bun was moved from Zig to Rust after years of stability work still left the project exposed to memory leaks, use-after-free crashes, double frees, and other failures. The remarkable part is not just that AI agents helped port more than 500,000 lines of code in 11 days. It is that the process required adversarial reviewers, workflow rules, compiler feedback, test suites, fuzzing, and human supervision. The productivity story and the verification story are the same story.

Education is the same problem with higher stakes. Jessica Blake’s Brown story in ‘Inside Higher Ed’ is not really resolved by better policing.

Roberto Serrano suspects much of his welfare economics class used AI on a take-home midterm, saw the average jump to 96 percent, then moved the final back in person and watched the average fall to 48.6 percent. Brown’s own GenAI report says “There is no way to check with 100 percent accuracy whether GenAI has been employed” and urges faculty to “de-emphasize punishment.”

Serrano ends with the opposite fear: “We cannot choose to become idiots.” Both are right. Students will use AI. My opinion is that the institution’s job is to reward good use, punish fake work, and test intelligence, familiarity with process, and familiarity with content. Using AI does not have to be cheating. But of course it can also be cheating. There is no future higher ed without AI, that is a pipe dream.

Teaching use of AI is why the forward-deployed engineering boom matters. Tomasz Tunguz says AI companies have committed $9.75 billion in 12 months to FDE teams because the bottleneck has shifted from model capability to enterprise deployment.

That is a staggering number, but it makes sense. Powerful models do not automatically know how a hospital, a bank, a manufacturer, or a media company actually works. Somebody has to sit with the customer long enough to translate capability into operating change.

Health care shows the trap. Bob Kocher, Brian Zhao, and Erin Duffy argue that AI may raise U.S. health care spending in the short to medium term unless payment models change.

Better tools can produce more visits, tests, prescriptions, referrals, drug discovery, monitoring, and administrative activity. In a bad incentive system, productivity can become more billable volume rather than lower cost. AI does not automatically fix institutions. It amplifies the rules it enters.

That is the deployment clock. Companies, schools, and health systems are learning how to use AI. Not demo it. Use it.

The third clock is medium term - capital and infrastructure.

Pavel Prata’s mega-fund chart is a useful warning. Fourteen funds represented only 6.7% of fund count but controlled 65% of all capital raised in the first half of 2026. Andreessen Horowitz alone raised $15 billion, more than the bottom 168 funds combined. Thrive added $10 billion. Two firms collected roughly one third of H1 2026 capital.

That is not a normal venture market. It is a capital-allocation machine being rebuilt around AI, defense, space, compute, and private-company duration.

Turner Novak’s secondaries post adds the liquidity side. VC secondaries have grown “from a $250M to $150B market over the past 25 years,” and one of the questions in that market is “what happens after SpaceX, OpenAI, Anthropic IPOs.” That is not a side question. It is the question of how private markets absorb companies that take longer to mature, require more capital, and create wealth before the public ever gets access.

Dan Gray calls venture the sick man of private markets because the fund model is showing strain. His proposed answer is not a retreat from ambition. It is a more serious financing model for reindustrialization: small funds to discover, venture philanthropy to support early strategic technologies, and giant pools of capital to fund deployment. That is probably closer to what the AI buildout needs than the old story of two engineers, a laptop, and a Series A.

Infrastructure says the same thing. M.G. Siegler’s “Elon Lever” is the observation that SpaceX and xAI turned surplus compute from a cost problem into a cloud revenue narrative. Chris Zeoli points out that networking is already 10% to 15% of cluster cost and that frontier runs often sustain under 50% utilization. Rebecca Kaden writes about data at the edge, where AI moves the software flywheel into the body, the ocean, robotics, infrastructure, weather, and ambient conversation.

In other words, AI is not becoming less physical as it gets more intelligent. It is becoming more physical. More data centers. More power. More networks. More robots. More sensors. More edge devices. More capital.

This is why the short-term bubble conversation can be true and still not be enough. Bubbles are about price. Buildouts are about capacity. The hard part is that both happen at the same time.

The fourth clock is long term - civilization.

Arvind Narayanan calls AI a “normal technology.” I like that phrase because it deflates hysteria without deflating importance. Electricity was a normal technology. The internet was a normal technology. Normal technologies do not change the world by magic. They enter institutions, change workflows, create new jobs, destroy old ones, and take longer than their loudest advocates expect.

Narayanan’s “decide, execute, deliver sandwich” is a useful framework. AI may compress the execution layer, but humans still decide what is worth doing, verify quality, integrate the result, and accept responsibility. That does not make AI small. It makes it adoptable. It also means the labor question is not simply “will AI replace jobs?” The better question is: which parts of work become cheaper, which parts become more valuable, and who owns the system of record when the change is finished?

John Battelle’s essay pushes this into life itself. He quotes Ian Bogost’s line that “our lives have become dematerialized” and asks whether software has eaten the world without anyone asking what the meal costs. That is not anti-technology. It is a humanist question. If every layer of experience is mediated through “smoothed glass and pixels,” then abundance cannot just mean more computation. It has to mean better life. Actually more computation may be the only way to get to a better life.

The Eventbrite story belongs here too. The internet did not replace real-life gathering. It made discovery easier, ticketing easier, payments easier, promotion easier. But the thing people wanted was still physical presence. That is an important corrective to the pure digital story. Humans still want to be in rooms together. Less time spent earning a wage will facilitate that.

Noah Smith asks whether America’s 250th anniversary is really about the end of “the human age.” Ivan Krastev asks why America has lost faith in itself. Krugman complicates the lazy Europe-versus-America story by noting that Europe still offers more leisure, lower inequality, and longer life expectancy even if it has missed the AI boom.

Matthew Yglesias brings it home through housing. Capitalism is hard to defend to young people when the thing they need most is made scarce by law. If private ownership exists inside a system where building is blocked, delayed, and rationed, people experience the result as failure. They are not wrong to notice.

This is where last week’s theme - Universal Basic Capitalism - fits. Andrew Keen framed the question as whether citizens should become shareholders in AI-created wealth rather than recipients of welfare managed by a larger state. That was his summary of last week’s show.

He quotes my line from the interview: “The pinnacle of capitalism is still flawed. Any idea that it’s perfect - this idea of the perfect union - is deeply flawed as a concept and always has been.”

That is the point. The answer to capitalism’s flaws is not to pretend they do not exist. Nor is it to abandon the wealth-creation machine just as it is about to become more powerful. The answer is to make ownership broader, make deployment real, make institutions faster, and make the benefits visible in ordinary life.

Sam Altman’s proposed 5% public stake in OpenAI belongs in this argument, whether one likes the mechanism or not. The Wall Street Journal frames it as “more regulation, more taxation and even partial government ownership.” Maybe that is right. Maybe it is too clever by half. But the instinct behind the debate is real: if AI creates extraordinary wealth and dislocates work, the ownership question cannot be left until after the fact.

There are political risks in having civilizational opinions. The Wall Street Journal’s other OpenAI and Anthropic piece makes the useful distinction. Anthropic’s fight with Washington is acute: access, procurement, military use, and national-security suspicion. OpenAI’s exposure is more structural because it is becoming a consumer platform, enterprise vendor, national infrastructure candidate, and geopolitical asset at the same time. Companies that become that important do not get to remain merely companies. They become political objects.

That is why the ownership question matters. If AI companies are going to be treated as infrastructure, if their models shape work and education, if their compute becomes a national asset, and if their wealth creation is large enough to change the distribution of opportunity, then the social contract cannot be an afterthought. The point is not to nationalize intelligence. The point is to make sure the wealth-creation machine produces citizens with more agency, not only institutions with more power.

So the issue is not whether AI is a bubble or a revolution. It is both, on different clocks.

In the first clock, prices and valuations are moving faster than certainty. In the second, deployment is colliding with institutions. In the third, capital and infrastructure are reorganizing around the buildout. In the fourth, the question is whether all of this produces better lives, more freedom, and a civilization that knows what to do with abundance.

That last word still matters. Abundance is not just GDP. It is not just model capability. It is not just cheaper tokens. Abundance is economic success plus life experience plus personal freedom. It is the capacity to build, to own, to move, to gather, to work, to learn, and to live better.

The AI economy has multiple clocks. The mistake is reading only one of them.

Post of the Week notes the passing of David Potter. I first met David in 1996 when EasyNet was about to be listed on the AIM market in London. We were seeking investment from his very successful company - Psion. We didn’t get it :-)

David was an entrepreneur and innovator. He was deep in science, very opinionated, and intensely aware of opportunity. In later life, due to family connections, I got to know him quite well. He will be missed, but his impact on the history of technology is permanent.